Everything You Need to Know Before Applying for Alt A Loans

Everything You Need to Know Before Applying for Alt A Loans

Blog Article

The Benefits of Alt A Loans: A Smart Choice for Home Purchasers

Alt A finances have emerged as an engaging option for home customers browsing diverse monetary landscapes. Understanding the intricacies of Alt A fundings and their ramifications for lasting monetary health is important for prospective customers.

What Are Alt A Loans?

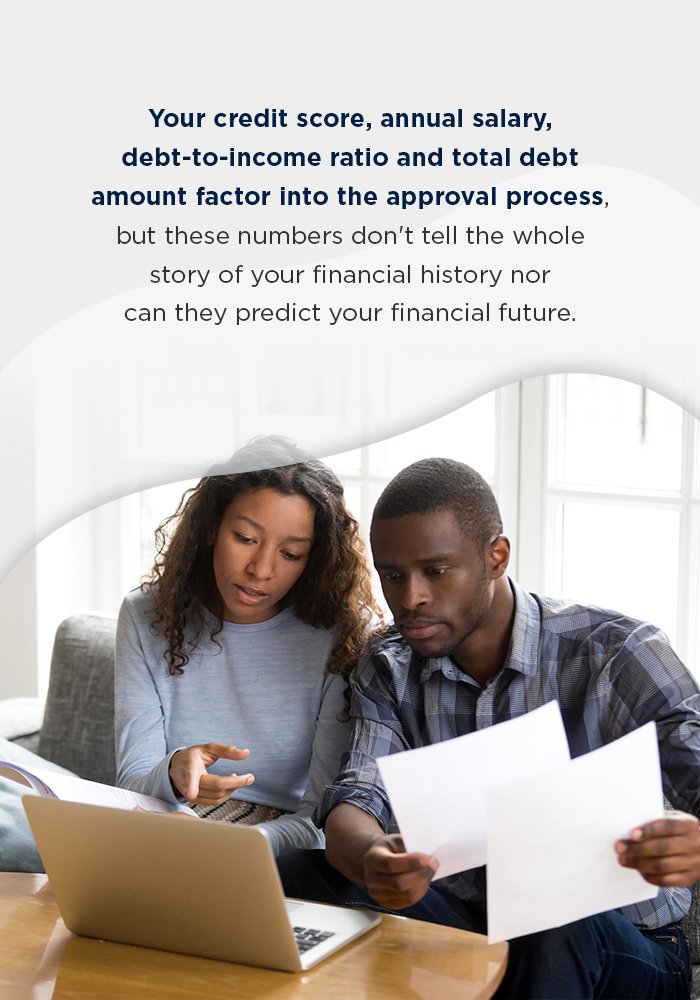

The underwriting standards for Alt A lendings frequently enable more versatile documentation, though they typically need a higher credit history than subprime car loans. Customers seeking Alt A financing may gain from reduced rates of interest compared to subprime options, making them an appealing selection for those aiming to refinance a home or purchase without fulfilling the complete requirements of prime car loans.

These car loans can provide competitive terms and are made to link the space for customers that are taken into consideration as well risky for prime lendings yet as well stable for subprime loans. Thus, Alt A finances can be an efficient solution for customers who need a home mortgage product customized to their certain financial conditions.

Adaptable Qualification Needs

One of the specifying features of Alt A loans is their versatile qualification demands, which provide to a broader array of borrowers. Unlike standard lendings that usually impose rigid criteria, Alt A finances are designed for individuals that might not fit the conventional mold yet still possess the financial ways to take care of mortgage repayments. This versatility is specifically advantageous for freelance people, consultants, or those with non-traditional income sources, as it enables them to present alternate documents to verify their profits.

Eventually, the versatile qualification needs of Alt A fundings empower a varied range of consumers, supplying them with the opportunity to protect financing for their dream homes despite their special financial circumstances. This inclusivity is a significant benefit in today's evolving real estate market.

Reduced Down Repayment Alternatives

Typically interesting many home buyers, reduced down payment choices related to Alt A loans make homeownership more attainable. Unlike standard fundings that frequently call for significant deposits, Alt A lendings normally allow purchasers to safeguard funding with a deposit as low as 10% and even much less in some cases. This versatility can be specifically beneficial for novice home purchasers or those with minimal financial savings, as it reduces the preliminary monetary problem.

Reduced deposits enable buyers to enter the housing market sooner, permitting them to capitalize on desirable market problems and property worths - alt a loans. In addition, this alternative can assist individuals who may have a strong revenue yet do not have considerable liquid assets to gather financial savings for a larger deposit

In addition, reduced down repayment demands can be beneficial in competitive markets, where bidding process battles typically drive prices higher. Home buyers can act promptly without the prolonged timeline usually needed to conserve for a larger deposit. On the whole, the reduced down payment alternatives used by Alt A finances supply a viable path to homeownership, making it an appealing choice for several potential customers.

Affordable Rates Of Interest

Along with decrease down repayment options, Alt A finances are understood for their affordable rates of interest, which even more boost their attract home customers. These finances generally supply rates that are extra positive contrasted to standard mortgage products, making them an eye-catching option for those aiming to finance a home without the rigid needs of prime fundings.

The affordable nature of Alt A funding passion rates can dramatically lower the overall expense of loaning. For home buyers, this equates right into lower month-to-month payments, permitting better budgeting and financial preparation. Moreover, when rate of interest are reduced, customers can certify for greater lending amounts, broadening their alternatives in the real This Site estate market.

Furthermore, the rate of interest on Alt A loans can be particularly useful in a changing economic situation, where keeping a reduced price can shield borrowers from rising costs. This benefit makes Alt A loans a strategic choice for individuals that focus on price and monetary versatility. Eventually, the competitive interest rates related to Alt A loans not just boost the purchasing power of consumers but also add to an extra easily accessible and diverse real estate market for prospective property owners.

Ideal for Unique Economic Circumstances

Navigating the intricacies of home funding can present obstacles, particularly for purchasers with unique economic circumstances. Alt A car loans cater particularly to individuals that try this web-site may not fit the typical loaning criteria, making them an eye-catching choice for diverse economic profiles. These lendings typically offer borrowers that are self-employed, have uneven income streams, or have non-traditional credit rating.

Among the essential benefits of Alt A car loans is their adaptability in earnings confirmation. Unlike conventional finances that require substantial documentation, Alt A finances frequently permit for stated income or alternate paperwork, simplifying the application procedure. This adaptability helps purchasers that may encounter difficulties verifying their economic security through standard methods.

Furthermore, Alt A financings can accommodate higher debt-to-income proportions, which can be beneficial for buyers with considerable existing commitments yet dependable earnings resources (alt a loans). This inclusivity opens homeownership possibilities for many who may otherwise be omitted from the marketplace

Conclusion

Finally, Alt A car loans provide significant advantages for home customers, specifically those encountering non-traditional monetary situations. The flexible qualification needs, reduced deposit options, and competitive passion rates make these car loans an Read Full Article attractive alternative for varied consumers. By fitting distinct financial scenarios, Alt A finances assist in access to homeownership, encouraging individuals to navigate the real estate market with greater convenience and protection. This financing alternative plays a vital role in advertising inclusivity within the realty landscape.

Alt A lendings have actually arised as a compelling choice for home customers navigating diverse economic landscapes.Alt A lendings, or Alternate A-paper loans, represent a group of mortgage financing that falls in between prime and subprime fundings. Unlike typical car loans that commonly enforce stringent requirements, Alt A finances are designed for individuals who may not fit the traditional mold and mildew yet still have the financial means to handle home mortgage settlements. Unlike traditional car loans that commonly call for significant down payments, Alt A car loans usually enable purchasers to safeguard funding with a down settlement as low as 10% or even less in some situations. Unlike traditional finances that call for substantial paperwork, Alt A fundings frequently allow for stated revenue or different documentation, simplifying the application procedure.

Report this page